Where Do You Underwrite the Next Space City?

The case for Denver, Austin, Huntsville — or 1,000 space cities.

First, weigh in:

Which city do you think wins the next era of the U.S. space industry? Vote in the poll, then read on for our case for each — and one argument that none of them wins outright.

We’ll get to the case for each city in a minute. But before we do, the reason we’re even asking the question this way — city by city, rather than “is space a good sector” — is because the next phase of this industry is going to be decided on the ground. Literally.

Why space (the unearthly kind) should matter to real estate investors

If you underwrite industrial, flex, or land in any of the cities we’re about to discuss, the next space cycle is going to bend two things at once — and only one of them is the obvious one.

The obvious one is acreage. As Lauren and Lucy put it on the episode, the next phase of the industry is going to look like an acreage takeover. Space companies need testing land, manufacturing campuses, secure perimeters, future expansion room, and proximity to power and logistics. Starlink in Bastrop, Blue Origin’s broader Texas footprint, Firefly’s Rocket Ranch — these are not coastal launch sites. They are industrial site selections that happen to be aerospace. Wherever the next cluster compounds, large contiguous parcels with the right zoning and power story get repriced first.

The less obvious one is asset spec. A satellite manufacturer is not a beverage distributor. A propulsion test cell is not a logistics warehouse. Space-tenant buildings need higher clear heights for spacecraft handling, heavier floor loads, ITAR-compliant secure facility build-outs, exotic-gas storage, and in some cases the ability to fail loudly without a HOA complaint. If you own a vanilla Class B industrial park, you should know whether you’re a credible landing spot for this tenant base, or whether your competitor down the road just spent the capex that you didn’t and is about to sign a 15-year lease at a rent you can’t match.

So the underwriting question is not just where the industry goes. It is which submarkets quietly become the credible candidates for the build-out, and which submarkets — even in the winning metro — get skipped.

With that as the backdrop, here’s where we think the space industry lands.

Where the space industry lives on Earth

There is something ironic about asking where the space industry should live.

Space, as an industry, is supposed to be the least place-bound thing imaginable. The whole point is to leave Earth. The product is orbit. The ambition is the Moon, Mars, satellites, habitats, space manufacturing, data centers in orbit, and possibly someday a real estate investment memo for a crater with excellent views of the moons.

And yet the space industry has always been deeply geographic. When America went to the Moon, we did not just build rockets. We built a geography of space on Earth: launch on the Florida coast, mission control in Houston, aerospace design and manufacturing in Southern California, rocket propulsion and engineering in Huntsville.

Those choices shaped where talent accumulated, where suppliers formed, where universities adapted, where capital knew to look, and where local identity attached itself to an industry. Houston did not become “Space City” because someone at the chamber of commerce workshopped a punchy tagline (although yes, yes they did). It became Space City because a very specific set of federal dollars, political relationships, institutional decisions, and land donations landed there and then compounded for decades.

That is the Build Order lesson hiding inside the space race: once an industry lands somewhere, it creates gravity. Talent moves there. Suppliers follow. Universities adapt. And then, decades later, everyone explains that of course it had to happen there.

So the question is not whether Houston and Los Angeles are space cities. They already are. Houston owns the mission-control mythology. Los Angeles owns the aerospace and Space Beach ecosystem. Cape Canaveral owns launch.

The real question is what city gets to be next.

Follow the money

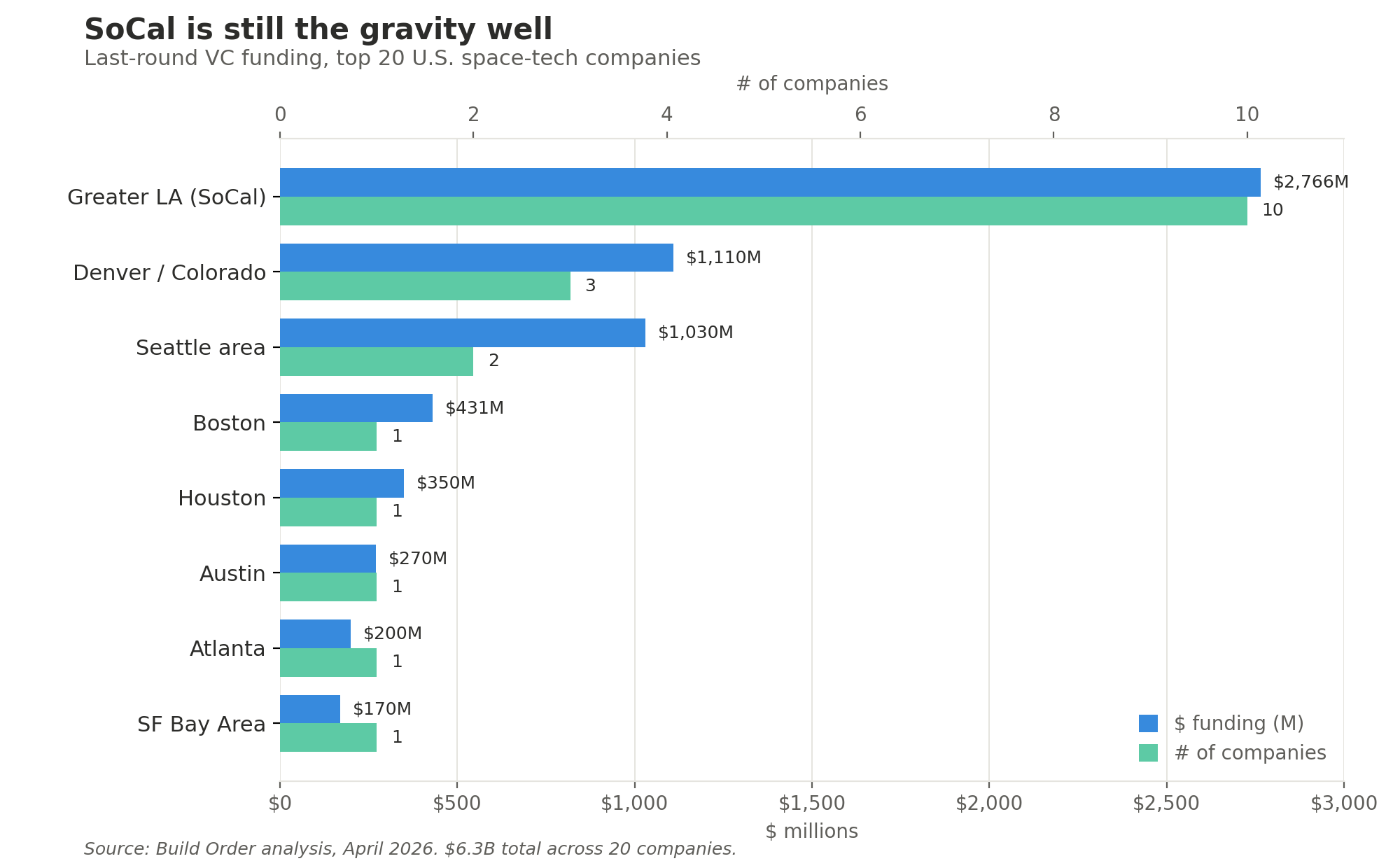

Before we go city by city, look at where private space capital has actually pooled.

We pulled the last funding rounds for the top 20 U.S. space and aerospace startups (Build Order analysis, April 2026). The picture is more concentrated than the “space is going everywhere” narrative suggests:

Half of the top 20 sit in Greater LA. Greater LA accounts for 44% of the dollars. If you broaden out beyond the top 20, the share of companies tilts even harder to SoCal. The capital concentration is more even — partly because the biggest single round in the list (Stoke Space, $860M) is in Kent, Washington — but the headcount story is unambiguous: founders are still picking Southern California.

The interesting question is what the next 20 looks like. And that is where the case for Denver, Austin, and Huntsville actually lives.

The case for Denver: The next space city that may already be one

If I had to make the most buttoned-up case for the next space city, I would probably start with Denver. Or more specifically, the Denver / Colorado Springs / Centennial corridor.

The Air Force selected Denver for missile development in the 1950s. NORAD is in Colorado Springs. U.S. Space Command has been based there, even as its long-term location has become a political football. Lockheed Martin, Boeing, Northrop Grumman, BAE, and a meaningful base of aerospace and defense talent are already there. The funding data backs it up — Sierra Space, Boom Supersonic, and True Anomaly together have raised over $1.1B, and they all sit within an hour of each other.

Denver has one of the things every would-be space city wants: an established pool of people who already know how space and defense work. That matters because space is not software in the pure “two people in a room and a GitHub repo” sense. It is physical. It is regulated. It is expensive. It touches national security. It has long procurement cycles. It requires people who know how to work with the government, design around failure, and build things that survive environments humans very much do not survive.

The case against Denver as the “next” space city is almost too flattering. Maybe it isn’t next because it is already one. Denver isn’t trying to become a legitimate space city contender. It is legitimate.

But that may also make it the strongest contender. If the next era of space is more defense-oriented, more satellite-oriented, more command-and-control-oriented, and more tied to national security, then Denver is very hard to ignore.

Denver’s biggest weakness may be that its story is not as clean. Austin gets to say “the next frontier is moving to Texas.” Huntsville gets to say “we are Rocket City.” Denver has a more diffuse claim with defense, aerospace, command, satellite talent, established contractors, startups, and Colorado Springs next door. That may not fit as neatly on a bumper sticker, but industries do not actually care about bumper stickers. They care about whether the right people, institutions, contracts, and facilities are nearby.

By that standard, Denver is a very serious answer.

The Case for Austin: “Sat” City

Austin’s best claim may not be that it becomes the next Space City. It may be that it becomes the next “Sat” City.

Lucy coined that phrase in the episode — or at least independently coined it, which in startup terms means we are treating it as canon. Sat City is short for satellite city.

It works because Austin’s space story is not really about replacing Houston. It is not about becoming the next Cape Canaveral. It is not even necessarily about unseating Southern California as the deep aerospace design cluster. Austin’s argument is more specific. It is about satellites, dual-use technology, manufacturing, software, hardware, defense, autonomy, communications, and all the strange overlap between space and the industries Austin already likes to think it is good at.

Starlink has a growing presence in the Austin orbit, especially around Bastrop. Blue Origin has been tied to a major manufacturing and logistics footprint. Firefly Aerospace has its Rocket Ranch. CesiumAstro is the only Austin company in the top 20 by funding ($270M raised, per our analysis), and it sits right in the middle of the satellite-comms thesis. Icon, which started as a 3D-printed housing company, is suddenly not just a proptech company but a “maybe we need to build on the Moon someday” company.

That is a very Austin sentence. A company starts with houses, ends up working on lunar habitats, and somewhere along the way everyone insists this was the plan.

Four reasons Austin shows up

First, land. Space companies need room. Not always launch-site room, but manufacturing room, testing room, logistics room, secure facility room, future expansion room. The real estate matters. The acreage matters. The ability to assemble sites matters. If you are building satellites or spacecraft components or dual-use manufacturing facilities, you do not necessarily need to be on the coast. But you do need space, power, labor, logistics, and a political environment that is at least plausibly excited about the fact that you exist.

Second, talent. Austin does not have Southern California’s aerospace bench, and pretending otherwise would be silly. But it has tech talent, startup talent, business talent, UT, and a growing base of people who want to live here and build here. It also has the classic Austin advantage of retaining graduates who historically had to leave to find certain kinds of ambitious jobs. If a space startup wants access to young technical talent before that talent gets absorbed into the existing aerospace establishment, being close to UT is not a bad strategy.

Third, adjacency. Austin is close enough to Houston’s NASA ecosystem, close enough to SpaceX’s broader Texas footprint, close enough to semiconductor and defense talent, and close enough to the state’s political and economic machinery to matter. It also sits in a state that has already become central to SpaceX’s geography: McGregor for testing, Boca Chica / Starbase for launch, Bastrop for Starlink, and Austin as a corporate and talent hub.

Fourth, myth. Austin has had a lot of myth precede reality. Tech moved here before every part of the tech ecosystem was here. Venture capital came later. Headquarters came later. Serious talent density came later. The story pulled some of the facts into existence. Space may be doing something similar.

If enough founders, engineers, investors, and operators believe Austin is where the next layer of space gets built, the belief itself becomes part of the infrastructure.

The case for Huntsville: Never bet against Rocket City

Huntsville is the funny one because it is both legacy and underappreciated.

It has Marshall Space Flight Center. It has the Army and defense infrastructure. It has rocket propulsion history. It has Space Command momentum. It has a name — Rocket City — that is almost too on the nose. The funding data doesn’t capture Huntsville’s real footprint, because most of what gets built there is on government contracts, not venture rounds. Performance Drone Works ($110M, just outside the top 20) is the rare exception.

If you are looking for the “next” space city in the sense of the next cool startup migration story, Huntsville may not be the obvious pick. It does not have Austin’s tech migration mythology. It does not have Denver’s mountain-west defense corridor brand. It does not have Los Angeles’ founder-mafia density or Houston’s Apollo-era mythology.

But if you are looking for durable space infrastructure, technical depth, government adjacency, and a city that has already absorbed the weirdness of being a place where rockets are normal, Huntsville belongs in the conversation.

The mistake would be assuming the next era of space only belongs to coastal venture-backed startup clusters or shiny tech migration markets. The next era of space will still involve government. It will still involve defense. It will still involve propulsion, testing, procurement, and the unglamorous but essential work of making the thing actually work.

Huntsville knows how to do that. And in an industry where the unglamorous work is often the difference between science fiction and launch, that is not a small thing.

So, who wins?

The annoying but probably correct answer is that it depends on what we mean by “space city.”

If we mean the next major defense and aerospace command hub, Denver may already be winning. If we mean the next satellite and dual-use manufacturing hub, Austin has a very real claim. If we mean the next place where propulsion, engineering, federal programs, and serious rocket people continue to compound, Huntsville is right there, quietly judging everyone who just discovered space because it became a venture category.

But I am not sure the next era of space produces one new Houston.

The 1960s space economy was massive, complex, heroic, political, and expensive, but it was still oriented around a relatively concentrated national objective: beat the Soviets, get to the Moon, prove the system could do it. Today’s space economy is broader and weirder. It is launch, satellites, communications, defense, Earth observation, lunar construction, space manufacturing, robotics, human health, materials, financing, procurement, secure facilities, and probably eventually a deeply cursed debate about whether orbital storage should be valued on a cap rate or a revenue multiple.

The industry is too multidisciplinary to live in one place. The better question may not be “which city becomes the next Space City?” It may be “which city wins which layer of the stack?”

Denver may win defense and command. Austin may win satellites and dual-use hardware. Huntsville may keep winning propulsion and federal engineering. Houston keeps human spaceflight. Los Angeles keeps design depth and aerospace founder density. Cape Canaveral keeps launch.

And then there are the other cities we are probably not paying enough attention to yet: Seattle, Phoenix, Albuquerque, Washington, D.C., San Antonio, Dallas, San Diego, the Florida Space Coast, and places that do not yet have the right myth.

That is the more exciting answer. Not one Space City. A thousand space cities.

Not because every city will launch rockets or build satellites or 3D-print houses on the Moon. But because the space economy is becoming less like a single mission and more like an industrial platform. Industrial platforms spread. They specialize. They attach themselves to existing strengths. They create new real estate needs, new talent pipelines, new supply chains, new politics, and new local identities.

The future of space will still be about leaving Earth.

But the future of the space industry will be decided by places on Earth.

And that, conveniently, is the whole point of Build Order.

This essay grew out of a Build Order conversation. If you haven’t caught it yet, you can watch all our episodes on all your favorite platforms: Substack, YouTube, Spotify, Apple Podcasts, Pocket Casts, iHeartRadio, and Overcast.